All Categories

Featured

Table of Contents

Dear Liz: When is the "pleasant area" for me to begin receiving Social Protection benefits? I am retired and accumulating two federal government pensions mine and my ex-husband's. I paid right into Social Protection for 26 years of significant profits when I remained in the economic sector. I do not want to go back to function to reach thirty years of considerable profits in order to stay clear of the windfall removal arrangement decrease.

I am paying all of my expenses presently but will certainly do even more traveling when I am collecting Social Security. I think I need to live up until concerning 84 to make waiting a great choice.

If your Social Safety and security benefit is genuinely "enjoyable money," as opposed to the lifeline it functions as for a lot of individuals, optimizing your advantage may not be your top concern. However obtain all the info you can concerning the expense and benefits of asserting at different ages prior to making your choice. Liz Weston, Certified Financial Planner, is an individual financing writer for Inquiries may be sent out to her at 3940 Laurel Canyon Blvd., No.

Cash value can collect and expand tax-deferred inside of your plan. It's important to keep in mind that superior plan fundings accumulate passion and minimize cash worth and the death advantage.

However, if your cash worth falls short to grow, you may require to pay higher costs to keep the plan effective. Policies might supply various options for growing your cash money value, so the attributing price depends upon what you pick and exactly how those options carry out. A set segment gains rate of interest at a defined rate, which may change gradually with economic conditions.

Neither kind of policy is always far better than the various other - everything boils down to your goals and strategy. Entire life policies might attract you if you like predictability. You know specifically just how much you'll need to pay annually, and you can see how much money value to expect in any kind of given year.

Iul Agent Near Me

When assessing life insurance policy requires, review your long-lasting objectives, your current and future expenses, and your desire for safety and security. Discuss your objectives with your representative, and pick the plan that functions finest for you.

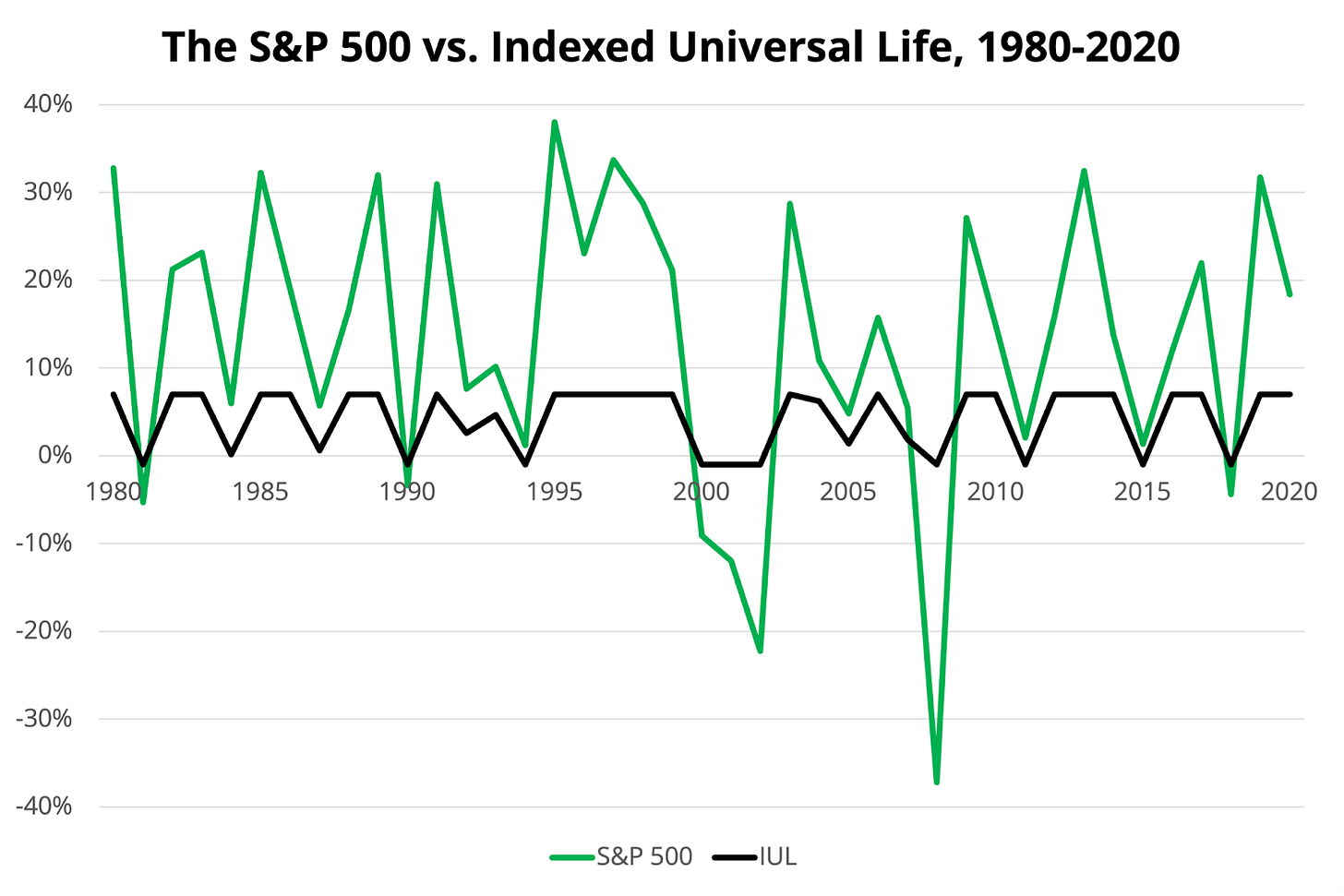

For example, in 2015 the S&P 500 was up 16%, however the IULs growth is capped at 12%. That does not sound regrettable. 0% flooring, 12% prospective! Why not?! Well, a pair points. First, these IULs neglect the existence of rewards. They check out just the modification in share rate of the S&P 500.

Iul Insurance

Second, this 0%/ 12% video game is generally a shop technique to make it seem like you always win, yet you do not. In the last 40 years, the S&P 500 was up 31 years. 21 of those were more than 12%, balancing almost 22%. It transforms out losing out on the massive development injures you way more than the 0% drawback helps.

If you need life insurance, purchase term, and spend the remainder. -Jeremy via Instagram.

Your existing browser might limit that experience. You might be using an old internet browser that's in need of support, or setups within your web browser that are not compatible with our website.

Your current browser: Spotting ...

You will have to provide certain give specific yourself regarding on your own lifestyle in way of life to receive an indexed universal life insurance quoteInsurance policy Cigarette smokers can expect to pay higher premiums for life insurance than non-smokers.

Universal Vs Term Life

If the plan you're looking at is generally underwritten, you'll need to finish a medical examination. This exam entails conference with a paraprofessional who will certainly get a blood and pee example from you. Both examples will be tested for possible wellness risks that could influence the kind of insurance you can obtain.

Some variables to think about consist of the amount of dependents you have, the number of earnings are entering your family and if you have costs like a mortgage that you would want life insurance policy to cover in the occasion of your fatality. Indexed global life insurance policy is among the much more complex kinds of life insurance currently available.

If you're looking for an easy-to-understand life insurance policy, nevertheless, this may not be your best choice. Prudential Insurance Coverage Firm and Voya Financial are some of the greatest providers of indexed universal life insurance policy.

Universal Life Insurance Loans

On April 2, 2020, "An Important Review of Indexed Universal Life" was provided via various outlets, including Joe Belth's blog. (Belth's summary of the original piece can be located here. His follow-up blog containing this post can be discovered here.) Not surprisingly, that piece produced significant remarks and criticism.

Some rejected my remarks as being "brainwashed" from my time helping Northwestern Mutual as an office actuary from 1995 to 2005 "regular whole lifer" and "biased versus" products such as IUL. There is no contesting that I benefited Northwestern Mutual. I appreciated my time there; I hold the business, its staff members, its items, and its mutual ideology in high respect; and I'm thankful for every one of the lessons I discovered while used there.

I am a fee-only insurance policy expert, and I have a fiduciary commitment to look out for the best passions of my customers. Necessarily, I do not have a prejudice towards any type of product, and as a matter of fact if I uncover that IUL makes feeling for a client, after that I have a responsibility to not just present but suggest that choice.

I constantly aim to put the very best foot onward for my clients, which suggests utilizing designs that reduce or get rid of payment to the biggest extent feasible within that certain policy/product. That does not always mean recommending the policy with the most affordable compensation as insurance is much much more difficult than merely contrasting payment (and sometimes with products like term or Guaranteed Universal Life there just is no commission flexibility).

Some recommended that my degree of passion was clouding my judgement. I enjoy the life insurance coverage industry or at the very least what it might and ought to be (single premium indexed universal life). And yes, I have an incredible quantity of interest when it concerns really hoping that the market does not obtain yet an additional shiner with excessively confident pictures that established customers up for dissatisfaction or even worse

Index Universal Life Insurance Calculator

I might not be able to change or conserve the industry from itself with regard to IUL items, and truthfully that's not my goal. I desire to assist my customers maximize worth and prevent critical errors and there are customers out there every day making bad decisions with regard to life insurance and specifically IUL.

Some individuals misconstrued my criticism of IUL as a covering recommendation of all things non-IUL. This can not be even more from the truth. I would not personally recommend the substantial bulk of life insurance policy plans in the industry for my customers, and it is uncommon to find an existing UL or WL policy (or proposal) where the visibility of a fee-only insurance coverage consultant would certainly not add considerable customer worth.

{kind=link}

Table of Contents

Latest Posts

Death Benefit Option 1

Index Ul Vs Whole Life

Seguros Universal Insurance

More

Latest Posts

Death Benefit Option 1

Index Ul Vs Whole Life

Seguros Universal Insurance